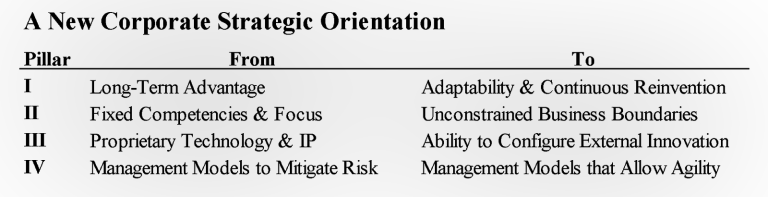

Four Pillars of Management to Guide Corporations Today

“The accelerated pace of product and market change will require that

tomorrow’s firm have wide-open ‘windows of perception’…a keen sense

of anticipation of potential threats from rival technologies and rival

firms…[and]the ability to make effective entrepreneurial decisions…”

In this time of digital transformation, these words could have been spoken by any of today’s Chief Executives. But this passage appeared in 19651 in a Harvard Business Review article written in by H. Igor Ansoff, a professor and mathematician the Economist refers to as the father of strategic thinking.

In his article, Ansoff was interpreting the impact of then-new computer and information technologies on the state of business and suggesting that corporations needed to manage themselves differently in the face of that change. “New technologies,” he wrote, “will continue to spawn new products and invade older technologies. . . life cycles of products will become shorter.” In order to appropriately respond to this kind of upheaval, Ansoff counseled corporations to institutionalize continuous R&D and make their organizations “flexible and responsive to changes…”

Uncertainty driven by technology has always changed business. But today is different. Today’s digital economy is defined by ever-accelerating waves of transformational technologies (data, AI, 5G, automation, etc.) and the consequent seismic impact those technologies are making in economics, industry structure, and the landscape for innovation.

Corporations are recognizing the far-reaching implications: “It’s been a long time since you could talk about sustainable competitive advantage. . .” Indra Nooyi, CEO of Pepsico has observed.

“The rule used to be that you’d reinvent yourself once every seven to 10 years. Now it’s every two to three years.” Jamie Dimon, CEO of JP Morgan, commented “there are hundreds of startups with a lot of brains and money working on various alternatives to traditional banking…They all want to eat our lunch.”2

What’s different from Ansoff’s time is not only the pace of change but the thorough power of new technologies to completely redefine the world. The central challenge is not merely that it is far more difficult to plan for change; it is forcing corporations to fundamentally rethink their place in evolving industries.

Toward (another) New Strategic Orientation

To succeed in this digital economy, corporations require a new strategic orientation. This refers to the competitive frame, planning perspective, management processes, and organizational structures corporations follow to drive performance; it is the set of tenets that underly how corporations approach what they do and how they do it.

From time to time, throughout history, the corporate world has needed to readjust its orientation—during the shift from the dominant agrarian to the industrial economy, during the introduction of DuPont Analysis and modern management techniques; and during the shift to the early information age.

Today we are in the midst of another inflection point. It is time again for corporations to adopt a new strategic orientation and pillars to live by.

Ironically, many of the themes Ansoff spoke of back in 1965 are new again. To be successful today, corporations need to re-learn Ansoff’s lessons. They need a renewed model of thinking around how to define the business, how to compete, how to execute—and how to regard what the corporation is meant to be.

We have worked with scores of corporations to help them shift to navigate this tumultuous new economic environment. Successful executive teams are adopting a new orientation based on four new tenets that explicitly address the opportunities and threats created by the digital economy.

1. Adaptability & Continuous Reinvention

From the earliest days of modern management, corporations have been pursuing strategies to drive sustainable competitive advantage. Born in a time when industries were stable and the cost to create assets was high, the concept of sustainable competitive advantage taught corporations to erect business models that offered long-term cost advantages, differentiation advantages, or both. As the industrial giants of the late 20th century demonstrate, those that were able to build these advantages could win over a long-term period. But beginning around the turn of this century the context for sustainable competitive advantage began to change. The cost of technology fell dramatically and technology innovation sped up. Digital-first business models sprung into being. Innovation ecosystems proliferated. We began to see product life-cycles shortening, industry lines blurring, and new, unexpected, competitors shaking up old markets. The kinds of conditions that once allowed for long-term advantage began to unravel. As Colombia Professor Rita Gunther McGrath observed, this was “the end of competitive advantage.”2

To succeed in today’s digital environment, corporations need to re-orient their management mindset toward one of adaptability and continuous reinvention. With this view, the corporation should no longer be thought of as a set of permanently-advantaged assets, but as an entity that continually configures solutions to ever-evolving customer needs. This is a fundamental change in the concept of the corporation and it changes the priorities for corporations in several important ways.

First, corporations should seek business model(s) that are flexible and platform-based. That means shifting from ones based on fewer long-term, owned/fixed assets to those based on flexible, 3rd party partnerships. It also means building technology- and business-platforms that enable the corporation to shift with agility from one market opportunity to the next.

Second, corporations should approach their offerings, competencies, and even business models as though they are temporary and adopt a continuous focus on change. Gone are the days corporations can ratify five-year strategic plans; business-building must now be a continuous process.

Third, in a world where markets and economics are changing quickly, corporations must continuously evaluate the economics of their portfolios and actively shift them—often in real-time. This ability to shift agilely across new investment opportunities will create more value than extending the lives of existing assets.

2. Unconstrained Definitions of Business Boundaries

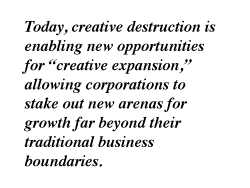

Creative destruction occurring in today’s digital economy is as much an opportunity for corporations as it is a challenge. Whereas new technologies threaten the businesses of incumbents, they also afford corporations significant new degrees-of-freedom for growth.

Time was, the cost and effort to develop differentiating technologies and competencies were so high they tended to lock corporations within a narrow set of boundaries. Yes, corporations could gain access to new technologies—but only through major acquisitions. But the innovation ecosystem has changed. Today, the kinds of technologies and competencies corporations require to grow into new arenas are, to a great extent, readily accessible in collaborations with a vast, growing, venture innovation ecosystem. Not only are new technologies within arm’s reach, but the cost to access (or acquire) them is now much more economically attractive.

Today, creative destruction is enabling new opportunities for “creative expansion,” allowing corporations to stake out new arenas for growth far beyond their traditional business boundaries. Corporations are free to define their businesses not by a fixed set of competencies, but by the value-maximizing role they may play for the market. Whatever capabilities and competencies corporations need to maximize that role can be accessed and assembled into the right value proposition. This ability to continually redraw business boundaries completely changes the game for corporations. (We wrote about this extensively, here). At the dawn of the information age, Ansoff anticipated the need for corporations to be able to “make bold and well-considered decisions outside their traditional product-market scope.”3 The ability to do so today is far more pressing.

3. Reliance on Ventures, Ecosystems, and Inorganic Innovation

Around the time of Ansoff’s article, technology innovation was owned mainly by large corporations and in corporate labs like Xerox Parc, Bell Labs, and others. At that time, 70 large industrial firms accounted for the vast majority of innovation in the United States. But by 2005, the share of large-firm R&D spending had fallen to 37%. And during the 15 years since then, a vast and sophisticated startup ecosystem has taken shape—dramatically expanding access to capital, guidance, and resources and improving the potency of small firm innovation. As many chief executives have observed, many of the most transformative industry innovations today are being driven by startups.

At the same time, the evolution of digital business models, digital platforms, enhanced connectivity (via API technologies, etc.) have together led to the rise in digital ecosystems. As we noted in these articles4,5, ecosystems are not merely a way to reach more customers, but can be a fundamental element of business models. They tend to feature low/zero relational and scale costs, abundant data, powerful network effects, and an efficient ability to expand value propositions. Where historically competitive advantage was built from assets, such advantage is increasingly built from ecosystem partnerships.

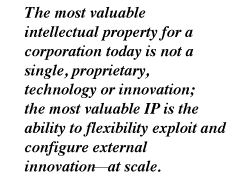

Taken together, the evolution of the startup- and digital -ecosystems have transformed the innovation and growth landscape for corporations. Today, virtually any technology, capability, or solution is available, accessible, investable and acquirable from the startup and digital ecosystems—and at an increasingly attractive relative cost and risk. Whereas corporations were historically forced to develop differentiating innovations organically, the digital era has opened up vast new external sources of growth and innovation—where startups, ecosystems and 3rd party solutions represent an increasingly compelling, if not dominant, share of the opportunity set. In some cases, external innovation may be the only viable option to pursue certain opportunities. This is a permanent shift of the innovation and growth landscape for corporations. To be successful today, corporations must seek external sources of growth and innovation. The most valuable intellectual property for a corporation today is not a single, proprietary, technology or innovation; the most valuable IP is the ability to flexibly exploit and configure external innovation—at scale.

4. Management Models Based on Startup Principles

The major management processes corporations follow today—Strategy, Resource Allocation, and Performance Management— were originally designed to accomplish two things:

1) extract long-term value from the core business

2) mitigate risk

Traditional management processes came into being at a time when business models were asset-intensive and expensive to build and when the context of the day incented corporations to erect and preserve a long-term competitive advantage. In turn, management processes prioritized stability, predictability, risk mitigation, and accuracy and they produced the kinds of hallmarks most managers are familiar with today: high-hurdles for capital investment, long planning horizons, low-tolerance for experimentation, and a low tolerance for failure. Over the years, investors came to expect the same; failure to deliver predictably stable growth in EPS meant poor stock market performance. As a consequence of corporations’ this stability-focused orientation, corporations were dis-incented to allocating capital to risky endeavors or moving meaningfully beyond the traditional business.

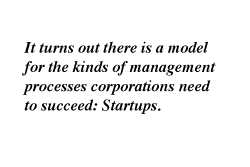

But to respond to the challenges and opportunities of today’s environment, Corporations need to manage themselves differently. It turns out there is a model for the kinds of management processes corporations need to succeed: Startups. Startups operate with agility and optionality. They prioritize experimentation and fast-cycle learning. They focus on continuous value engineering and actively evolve their businesses over time. And, importantly, the startup funding model deliberately stages capital investment, where large investments come only after strategies have had the chance to be proven.

Corporations can learn a lot from how startups manage themselves. In strategy, it means shifting from five-year planning to a focus on continuous, adaptive, market-responsive pursuit of new opportunities—what startups call “lean startup.” In resource allocation, it means shifting from annual capital budgeting to perpetual, options-based investments staged to successively prove and unlock value. In performance management, it means a focus on continuous learning, tolerance of failure, and the ability to embrace moving targets. The acceleration of technology means corporations must move beyond the anachronistic management processes of the past and design management infrastructures that support agility, flexibility and continuous renewal.

Bringing it all Together

The most foundational tool a Chief Executive has to shape the future of the company begins with the set of principles they follow to orient the company. Strategy, management, execution and culture all stem from those principles. The significant technology and economic shocks the digital economy is creating today require corporations once again renew their operating principles and orientation.

Just as Ansoff predicted in 1965, the winners of the future will orient the way they think and act based on entrepreneurial agility.

1. “The Firm of the Future” Harvard Business Review, by H. Igor Ansoff

2. “The End of Competitive Advantage, How to Keep your Strategy Moving as Fast as Your Business,” Rita Gunther McGrath, university press, 2010

3. “The Firm of the Future” Harvard Business Review, by H. Igor Ansoff

4. The New Corporate Growth Playbook in the Age of Digital Transformation Part II Corporate Development